I was deep into drafting this letter when the futures market began selling off on Sunday night, forcing me to pause and rethink much of what I had written. The recent market volatility has been truly extraordinary. On the upside, it’s led to my phone buzzing nonstop with calls, emails and texts from concerned friends and clients, a level of engagement that I appreciate.

On Monday, the Tokyo Stock Exchange Stock Price Index (“TOPIX”) experienced its worst day since 1987, serving as a stark reminder of the fragility of global markets. While we’ve weathered significant global storms such as COVID-19 and the global financial crisis, Monday’s plunge in the TOPIX was the most severe in nearly 40 years. Considering all that has transpired since 1987, it’s remarkable that Monday stands out as the worst day. Naturally, this turmoil spilled over into the U.S. markets, as global sell-offs often become contagious.

“Only when the tide goes out do you discover who’s been swimming naked.” — Warren Buffett

The U.S. market was already on shaky ground due to weak economic data, including disappointing labor and manufacturing reports, which stoked fears of a global economic slowdown. Many believe that the surprise rate hike by the Bank of Japan was the catalyst that ignited a broader market sell-off, shocking investors who had expected a continuation of low rates. This triggered a sharp decline in the equities of major Japanese trading firms, leading to turmoil across Asian markets and eventually cascading over globally. The interconnectedness of the global financial system means that events in one region can quickly affect markets worldwide. Specifically, many investors were short Japanese bonds to invest in higher-yielding assets elsewhere, and when a global shock occurs, those trades unwind violently. Of course, many apply copious amounts of leverage to this carry trade to increase returns. It’s a clear reminder that while markets tend to rise slowly, they often fall quickly—much like taking the stairs up and the elevator down.

When the sell-off begins and volatility spikes, it’s a risk-off scenario across most risk assets. This is largely driven by leveraged positions and risk management practices. In leveraged portfolios, increased volatility translates to increased risk, prompting managers to reduce their exposure. This often leads to the selling of the best-performing stocks or other assets, exacerbating the decline. At one point, the VIX surged over 60% on Monday, marking the highest level since the COVID-19 shutdowns. What happens next? My phone starts to buzz…

“If you put the federal government in charge of the Sahara Desert, in 5 years there’d be a shortage of sand.” — Milton Friedman

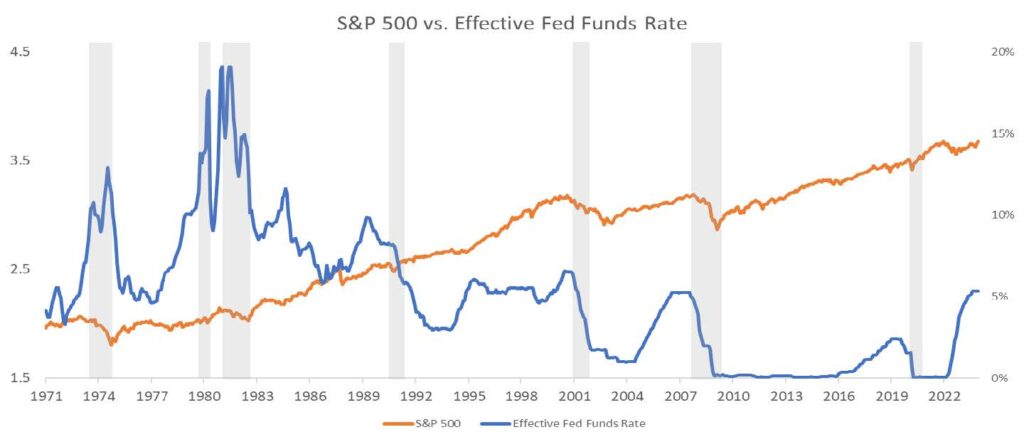

The unemployment rate is currently 4.3% and beginning to rise, but it remains well below the historical average of 5.7% over the past 70 years. The Federal Reserve, with its dual mandate to manage both inflation and unemployment, is now shifting its focus more towards the latter, as inflation appears to be under control at this juncture.

It’s important to note, however, that the current low unemployment rate might be somewhat misleading. Recent studies have shown that a significant portion of post-COVID job growth has been driven by immigrants. In fact, one study suggests that 75% of employment growth since 2019 has been attributed to this demographic.(1)

U.S. GDP has shown robust growth, with Q2 coming in at 2.8%, and the Atlanta Fed’s GDPNow currently estimating 2.9% as I write this. This is near the upper end of the healthy 2-3% growth range (see shaded area in the chart below). If this economy doesn’t feel like your typical growth environment, you’re not alone. Many have yet to fully adjust to the previous price increases, which still weigh heavily on consumer sentiment. Government spending has been a significant driver of recent GDP growth, fueled by the passage of the Inflation Reduction Act, the Infrastructure Bill, and the CHIPS Act. As these initiatives continue to roll out, we expect this trend to persist. Over the past six quarters, even if all other economic activity were stagnant, the economy would have still averaged nearly 0.7% GDP growth per quarter solely due to government spending.

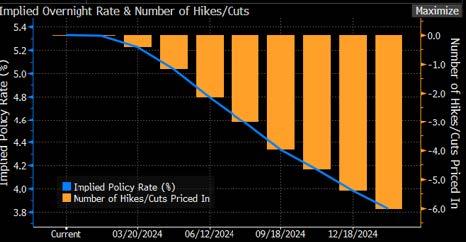

The market is currently pricing in five rate cuts by January 2025, with a 76% probability of a 50 basis point cut in September. Given rising unemployment and the difficult housing situation, I agree the likelihood of at least one rate cut in September is extremely strong. As I’ve highlighted in previous letters, the rate curve used to forecast these probabilities is highly volatile. We’ve witnessed market expectations fluctuate significantly—from anticipating seven cuts, down to just two, and now back to five—reflecting the uncertainty and sensitivity of market sentiment to evolving economic conditions.

Looking ahead, we have two more CPI and jobs reports scheduled before the next Fed meeting. If these data points align with recent trends, we can expect the much-anticipated Fed cuts to begin in September.

These rate cuts are particularly significant for smaller businesses. A compelling chart from Torsten Slok of Apollo illustrates the growing divergence between Large Cap (S&P 500) and Small Cap (S&P 600) companies following recent rate hikes. Smaller companies, which are more reliant on floating-rate debt due to limited access to capital, are particularly vulnerable to changes in interest rates. This sensitivity is clearly reflected in the data, highlighting the disproportionate impact that rate increases can have on smaller firms compared to their larger counterparts.

“If you don’t know where you’re going, you might wind up someplace else.” — Yogi Berra

So, where does this leave equity markets? They remain expensive. The S&P 500 is currently trading at 21.5 times forward earnings, nearly two standard deviations above historical norms. The bifurcation in small-cap performance, as highlighted by Torsten’s analysis, has led to significant underperformance of smaller-cap companies. Since January 2023, the S&P 600 has trailed the S&P 500 by almost 19%, underscoring the stark contrast in market dynamics between large and small-cap equities. While we expect that rate cuts could provide some relief to smaller companies, if we are indeed entering into a recession, the benefits of these cuts may be outweighed by the broader impact of a slowdown in economic activity.

An interesting trend to watch is the performance of the AI hyperscalers—Amazon, Microsoft, Google, Meta, and Tesla—who are leading the charge in AI development and capital expenditures. Last quarter saw a noticeable shift among investors, who are increasingly focused on when they will see tangible returns on their AI investments and what those returns will be. David Cahn of Sequoia Capital published a thought-provoking article titled “AI’s $600 Billion Question,” which I highly recommend. The key takeaway is that the gap between expected AI revenue and actual returns, given the enormous spending, has raised concerns about the profitability of AI models going forward. This situation has profound implications not only for the hyperscalers but also for the overall performance of the S&P 500. While I’m far from being an AI skeptic, it’s important to note that if the return on invested capital decreases, it logically follows that multiples should adjust downward, ceteris paribus.

Portfolio Updates

We’ve made significant and exciting changes in both our Autumn Lane Diversified Strategies and Autumn Lane Alpha Opportunities portfolios. We’ve added some outstanding managers and have been reallocating from others. Due to lock-up provisions, it will take a few quarters to see the full impact of these changes. However, we are excited and confident that our expected risk-adjusted returns should improve materially. We look forward to continuing to enhance the portfolio and generate alpha.

As always, if anyone has any questions or would like to discuss the markets further, please do not hesitate to reach out.

Best Regards,

Jim Mooney

Partner and Chief Investment Officer

Autumn Lane

DISCLOSURES

This information is provided, on a confidential basis, for informational purposes only and does not constitute an offer or solicitation to buy or sell an interest in Autumn Lane Partners, LP (the “Fund”) or any other security. It is intended solely for the named recipient, who, by accepting it, agrees to keep this information confidential. An investment in the Fund is speculative and involves substantial risks. Additional information regarding the Fund including fees, expenses and risks of investment, is contained in the offering memorandum and related documents and should be carefully reviewed. An offer or solicitation of an investment in the Fund will only be made to accredited investors pursuant to a private placement memorandum and associated documents. Interests in the Fund can only be purchased by investors meeting all the requirements of the Fund. There can be no guarantee that the Fund will achieve its investment objectives. The information contained in this material does not purport to be complete, is only current as of the date indicated, and may be superseded by subsequent market events or for other reasons. In preparing this document, Autumn Lane Advisors, LLC has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources.

This material may not be reproduced in whole or in part in any form, or referred to in any other publication, without express written permission. Send email requests to info@autumnlanellc.com.

(1) Center for Immigration Studies, June 10, 2024.